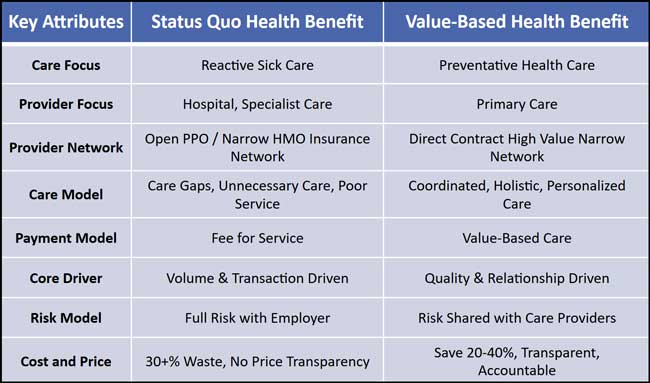

The key challenges with the status quo result from misaligned incentives not in the best interests of employers and employees.

Traditional health plans embrace Fee for Service (FFS) which doesn’t satisfy your employee needs. So it doesn’t provide competitive advantage in securing the best talent and keeping them healthy. These plans and FFS fall short in many ways.

- It provides reactive sick care that favors expensive hospital and specialist care. It marginalizes primary care that keeps patient healthy and prevents the need for expensive downstream care. Most patients lack strong primary care provider (“PCP”) relationships as they are often limited to 10 minute appointments once or twice per year and the wait to get an appointment can be several weeks.

- It pays for quantity of services rather than quality of care results. FFS incentivizes providers to deliver as much care as possible without holding them accountable for health results. Value-based care (VBC) rewards good health outcomes for lower cost and holds providers accountable.

- Physicians are unhappy with the FFS system because they spend more time filing insurance claims than treating patients. As a result, they are retiring early and worsening the physician shortage, particularly for primary care.

Status quo plans are unaffordable, gets more expensive every year, and consistently consume more company and employee resources. There is no earnest system strategy to contain costs because incumbents profit from FFS and price increases.

- Employer plans using status quo insurance carrier networks pay on average 250% of what Medicare pays for the same services. Medicare aims to pay cost plus a margin. Why pay so much more than Medicare?

- U.S. health systems mark-up their prices on average by 400% over cost and this can be 1000% or more for some care. This charge to cost ratio doubled since 2000 when it was 200%. Even with a 30-40% carrier network discount, the employer plan is still paying 250-300% over cost.

- Health systems and pharmacy benefit managers (PBMs) leverage pricing power they gained from market consolidation to raise prices every year even though demand and cost have remained largely flat.

- PBM’s opaque pricing contains significant price spreads, discounts and rebates that are not shared with the employer plan.

- Insurance carriers profit from price increases as they pass it along (after adding their margin) to employers and employees in higher premiums. For carriers’ underwritten business, ABA’s Medical Loss Ratio limits their ability to grow their profit margin via cost savings leaving them to primarily grow profit through price increases.

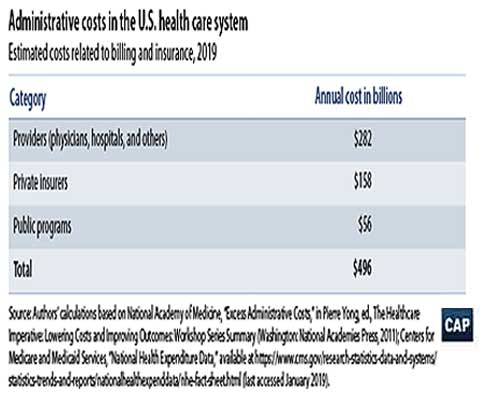

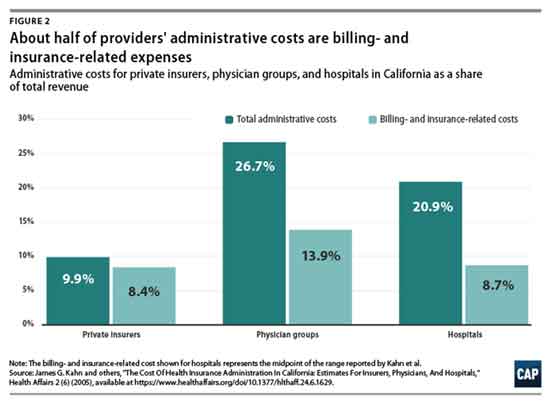

- Insurance carriers add significant administrative burden and cost (such as prior authorizations) with complex and laborious claim filing. Insurance billing and administrative cost amount to at least 10-15% of health care spend. And this doesn’t even include all the indirect cost related to billing such as the substantial time clinicians spend on documenting notes for billing that is passed through in provider pricing.

Employers provide health coverage for the majority of the U.S. population and can leverage their substantial collective spending power to change the system to benefit them and their employees. They need to drive the evolution to value-based care and health benefits. Contact us to learn how to make this transition.